Our Strategy and Insights Director Sarah Porretta tells a tale of love and pensions for International Women’s Day.

Are you sitting comfortably? Let me tell you a story, one that’s playing out in households across the UK right now:

Sam and Alex are thirtysomethings with two kids. They decided a few years ago it made sense for Alex to work part time, as the childcare fees were, more or less, equal to the drop in Alex’s net full-time pay. This pattern continues for a number of years and at the end of this period, the couple are finally persuaded to review their finances.

In this time, Sam’s salary has steadily increased through several promotions and job changes, and Alex’s has pretty much remained the same, but the couple are shocked to learn that Alex’s pension pot has accrued less than half of the value of Sam’s.

Alex hadn’t started paying into a pension until age 30, but those few years difference in payments have really widened the gap. Both of them had been focused on the money coming in and money going out as they raised two young children. Plus, with the freelance roles Alex took to fit around the kids, it wasn’t always easy to know how much was coming in, or to plan for the long term.

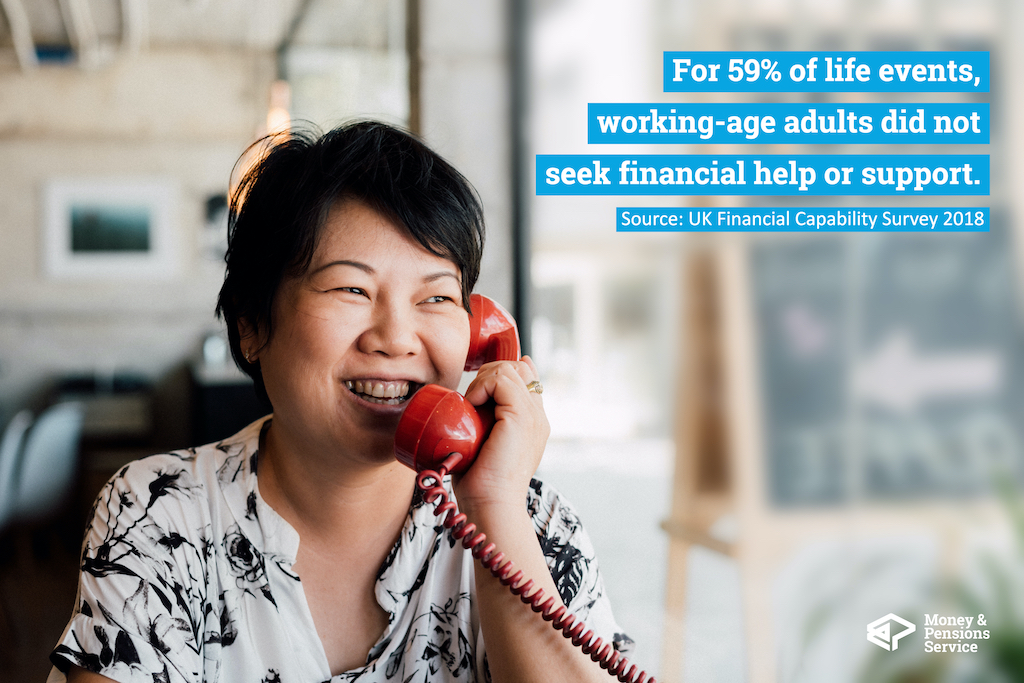

Sam had moved jobs several times before becoming a parent and even the thought of chasing up all those pensions and working out how much they were worth had always seemed so off-putting.

Neither had given any thought to their lifetime savings or the impact on their pension during parental leave, or when reducing Alex’s hours.

When they’d read guidance about going on parental leave and used online tools to work out their household budget over the years, the issue around pensions hadn’t really been flagged, so they’d missed it.

So is this a personal financial capability issue, an engagement issue, a financial guidance issue, or a products issue… or something else?

Well, most likely all of the above.

The pension penalty: a gendered or gender-neutral issue?

The astute among you will have noticed that I purposefully made the story gender neutral. This pension penalty for taking time away from work to play a caring role is still predominantly an issue that affects a greater proportion of women than men, but households are changing.

Alex and Sam’s situation is one that my husband and I found ourselves in – he’d worked part time while I was progressing my career and it was only when I came to move into my current role that I even thought about seeing what the impact had been on his pension. And it wasn’t good! There will be lots more couples in the same situation who haven’t yet realised the pension penalty one of them is paying, or what they could do about it.

Take up of shared parental leave is growing slowly, but growing; and the numbers of dads working part time and same-sex couples with kids are rising. So innovative thinking is required to level out outcomes for men and women across the board.

How design can make a difference

Imagine replaying that scenario and redesigning the world around Alex and Sam. What would you change?

Financial foundations: start young

You might, from childhood have financial education that equipped both girls and boys to hit those big life events fully prepared.

Engaged employers

These days you’d have auto enrolment, which might have meant Alex didn’t have those years of missed pensions earnings.

You might have them working in companies with proactive “financial health buddies” offering effective, well-evidenced guidance packages to help Sam and Alex start planning for the future and really exploring the options available to them when having children.

And offering engaging, tailored support for freelance or self-employed workers that’s widely known and well used.

Inclusive tech

You might want to ensure that there are really great tools available: a calculator that enables you to see in advance the impact of career breaks and reduced hours on your pensions. You might have a mid-life financial health check embedded and normalised across the UK.

You might have a pensions dashboard that would help you see all your pensions in one place and a really effective engagement programme that gets people using it.

Insightful data

You might have providers really starting to interrogate their data, and think deeply about whether product innovation is needed to better support households like Alex and Sam’s. You would hopefully have gender desegregation built into policy design to ensure nobody is left behind. You might find more products that nudge you to share your pension or liquid savings with your partner if one parent is reducing their hours, or just earns less.

I could go on, and I am sure you have so many more ideas yourself.

Innovative collaboration: the UK Strategy for Financial Wellbeing

This year, through the UK Strategy for Financial Wellbeing, over 100 senior leaders across the public, private and third sector are considering innovative solutions – such as some of those ‘imagined’ above – and making recommendations for how we can reach the five national goals laid out in the strategy by 2030.

I am delighted to be the Money and Pensions Service executive sponsor for the gender lens we have applied across the whole strategy, and excited to be working with a group of specialists from across industry to think about how we can level the playing field for men and women and recognise the benefits for everyone.

Learn more about the UK Strategy for Financial Wellbeing, and join the conversation on social media at #UKFinancialWellbeing. You can keep in touch via LinkedIn, Twitter and our monthly newsletter.