Debt Insight Manager Paul Das shares what we know about how many people need debt advice currently, who they are and how we are using these insights.

In September 2021, I explained how the Money and Pensions Service (MaPS) had adapted the way we measure the need for debt advice. This is a crucial activity for MaPS as understanding people who need debt advice is essential in formulating our plans to help them. This blog also set out some interim findings from our annual debt need survey looking at one of the groups within the measure.

With the survey now complete, we can now share what we know about how many people need debt advice currently, who they are and how we are using these insights.

What the debt need survey measures

Our debt need survey gives us insights on a broad cross section of society including ethnic minority, socially deprived and rural communities. We set detailed demographic quotas and weighting that accurately represent the UK population. We adopt a broadly consistent approach so that we can compare findings from year to year, but the survey evolves to keep us informed about changes in society such as different types of employment and the rise of new products and consumer behaviour. An example for this year’s survey being Buy Now Pay Later (BNPL) products.

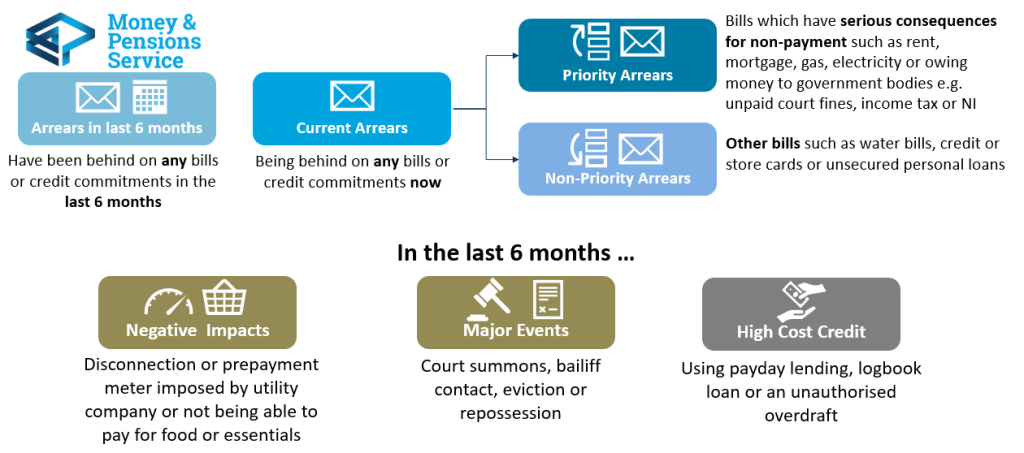

The new ‘need for debt advice’ measure

This figure shows the components that we use to allocate people to one of six groups in the measure. If you would like to know more about the criteria for each group, there’s more detail in our Need for Debt Advice explainer.

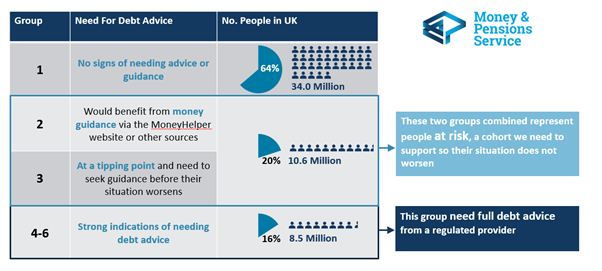

The size of each group in August-September 2021 when we ran the survey is shown below along with a description of each group’s need for debt advice.

- Most people in the UK (64% or around 34 million) were in group 1 and didn’t need debt advice despite the impact of the pandemic on the economy.

- A further 20% (around 10.6 million) were in groups 2 or 3 which we term ‘at risk’.

- However we identified that 16% (around 8.5 million) of the UK adult population needed debt advice.

How the pandemic changed the need for debt advice

Our unique role is to understand the national picture of local need. We’ve applied the new measure to the survey data from 2019 and 2020, so we can see how the proportion of people needing debt advice has changed from before the pandemic until now.

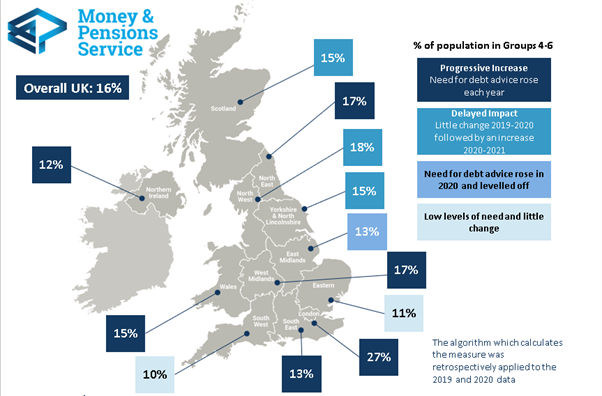

Devolved nation and regional need for debt advice

Every region and nation of the UK has seen an increase in the number of people needing advice since 2019, only the scale and timing is different. The regions marked in dark blue have seen increases in need each year while there was a delayed impact or different pattern in other regions.

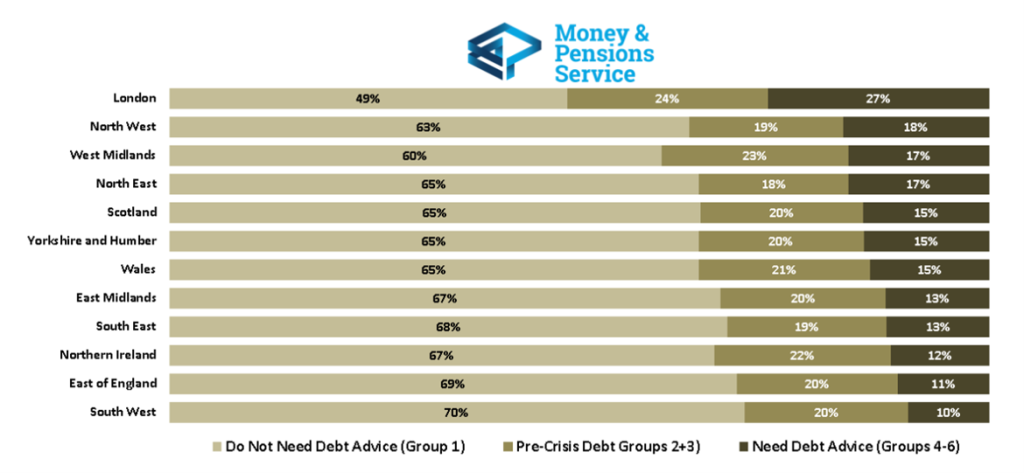

Need for debt advice across England

The concentration of need in London, the West Midlands and the North of England follows a similar pattern to studies on poverty and financial wellbeing carried out by other organisations. It reflects, among other factors, the concentration of private renters and higher cost of living in London and lower income levels in the midlands and the north.

Looking at all of the groups in the measure gives us a more complete picture including people at risk, who may “tip over” into the group needing debt advice. In each region and nation between one in five and one in four people are in this group.

London has the highest proportion of at risk people and this is on top of the highest proportion of people needing debt advice. The at risk group is also nearly as high in the West Midlands region.

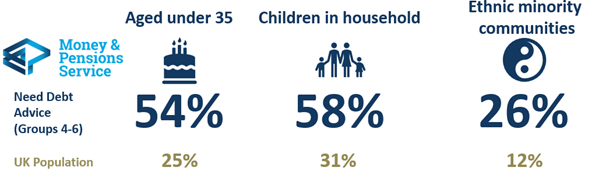

Profiles of people who need debt advice

We’ve looked in depth at the profile of people who need debt advice across a range of different characteristics. Here are the stand-out differences between them and the UK population as a whole, represented by all the people we interviewed in the debt need survey.

Age, ethnicity and family status

“UK population” percentages in the graphics are based on the results from everyone interviewed in the Debt Need Survey. Detailed demographic quotas and weighting were used that accurately represent the UK population.

People who need debt advice are more likely to be aged under 35 and have children. People from ethnic minority communities are more likely to need debt advice.

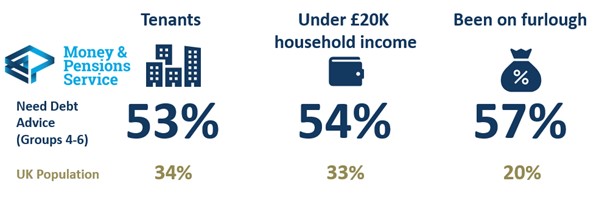

Housing and income status

People who need debt advice tend to be social or private tenants in low-income households (working, unemployed or retired), but this is not exclusively the case. People needing debt advice include homeowners on higher incomes. Many had been on furlough, or still were when we interviewed them at the tail-end of the scheme.

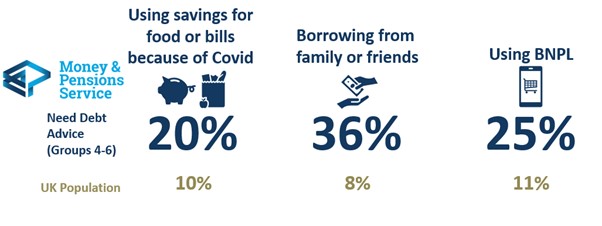

Household finances

People in need of debt advice are over four times more likely to be using informal borrowing from family or friends which does not show up in official figures such as those published by the FCA. A quarter are using BNPL services which often use less extensive credit checks than other forms of credit.

Life events, health and wellbeing

Looking at events that have happened to people needing debt advice gives us an insight into why they may be in this situation. They have often experienced more events that have a negative impact on their finances.

Other research carried out by MaPS indicates that people needing debt advice are likely to have low or very low financial wellbeing. However, our analysis of the impact of debt advice demonstrated that receiving advice raises financial wellbeing, has a positive impact on a client’s mental health and has wider economic benefits for society as a whole.

Whether someone needs debt advice or not, having a good level of financial wellbeing has a number of emotional benefits. It leaves people feeling in control, being able to pay bills and deal with the unexpected contributing to a better financial future.

How the survey informs our policy decisions

Learnings from the 2021 survey have allowed us to:

- inform funding decisions for debt advice in the devolved nations

- give early-stage feedback on HM Treasury’s Breathing Space Initiative

- share insights into BNPL customers for the FCA’s consultation on regulation

- pull together profiling information on users of illegal money lenders – an area where there is little published research, and

- profile people at risk of getting into problem debt and those who need debt advice now.

What’s next?

We will continue to use the new measure to monitor the need for debt advice in the UK and use the insights that we gain to inform our policy decisions and support the agencies we fund to deliver debt advice. We will produce more insight from this research over the coming months.

Keep up to date with our debt advice work: register for our monthly newsletter and join the conversation on LinkedIn and Twitter.