Debt Insight Manager Paul Das shares what we know about people using Buy Now Pay Later (BNPL) products, shares our concerns about what is currently offered by some providers and discusses how this product could fit within the regulated credit landscape.

BNPL in the UK

There are various estimates of the size of BNPL usage in the UK, but what all analysts and market commentators agree on is that its use is growing rapidly. FinTech companies led the charge in the UK, picking up Generation Z and Millennial customers born in the 80s and 90s. Growing up in an online world, these consumers were attracted by the ease of using this payment method, which is based on paying back credit in one or a series of interest free instalments over a fixed time period.

High-street lenders are now joining the market, either by designing their own versions of the ‘standard’ BNPL offer or adapting existing credit products to incorporate particular features.

The range of products available to purchase by means of BNPL is diversifying, with some providers now targeting their offer at those buying essential items, most notably groceries.

Who uses BNPL?

In March this year we published a blog about the need for debt advice in the UK based on analysis of our Debt Needs Survey. Looking at the data in more depth gives us insights about people who told us they have used BNPL in the last 6 months.

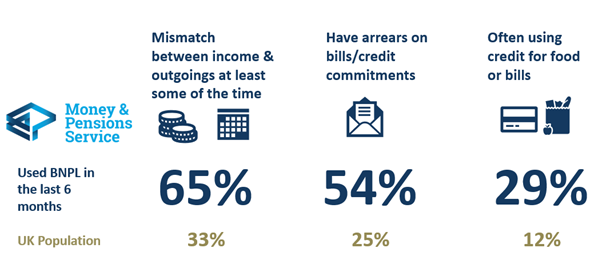

We found that BNPL users tended to be younger – 64% were under forty. This isn’t surprising – promotion of BNPL to date has typically targeted younger consumers buying fashion and lifestyle products, and BNPL is an accessible, immediate form of short-term credit for people under twenty-five who may have a thin credit file. As BNPL moves more mainstream, this may change.

BNPL has attracted people with a range of different household incomes. There’s a slight skew towards households with an income of under £20,000 per annum, but BNPL definitely isn’t focussed on low-income households. What we wanted to understand was the balance between customers across all providers between …

- People who have no arrears and will hopefully be able to manage BNPL along with other commitments and …

- Other cohorts who have problem debt to a greater or lesser extent

Taking all BNPL users together they do differ from the UK population in terms of their financial resilience.

They’re more susceptible to mismatches between bills arriving and the date that they receive their income. So, the ability to spread payments over time would make BNPL attractive.

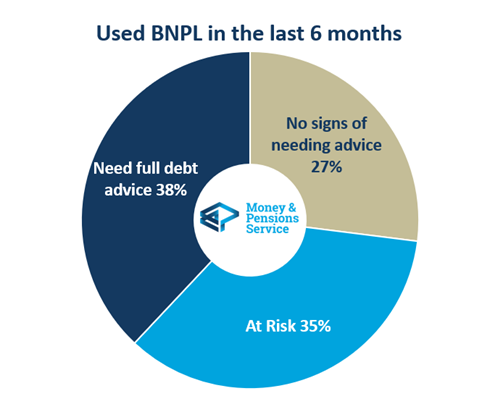

We’ve created a new measure of a person’s need for debt advice, there’s an explainer of how this works here. Analysing BNPL users according to this indicator, gives us the balance figures mentioned earlier:

This shows that nearly 4 in 10 of the BNPL users we interviewed need debt advice and a similar number are at risk of getting into that situation. That leaves just over a quarter for whom BNPL fits in well with their financial commitments.

MaPS’ concerns about BNPL

MaPS recognises that there is already good practice in the BNPL provider market. It can be a cheaper credit option for people who make all the payments when they are due and is more accessible for those who have a thin credit record.

But as the graphic above shows, BNPL customers include a substantial number who are already in problem debt. This suggests that up until now, BNPL has not been the right choice for some and there have not been sufficient checks to prevent this.

Some areas of concern:

- The light credit and affordability checks that are currently used for the product which, at best, tend to be limited to the customer’s history with the given provider. This makes BNPL an instant and superficially attractive solution to an affordability problem

- Lack of understanding of the product. A study carried out by the Consumers Association suggests that BNPL users are time poor and rate their confidence in managing money lower than those who did not use BNPL. This leads us to believe that many BNPL users are using this form of credit without completely understanding how it works

- Credit score invisibility. Although this an area under development, BNPL use is neither universally captured on credit files nor used to inform credit scores at present, so other creditors (including other BNPL providers) cannot get a full picture of a person’s overall credit use and behaviour

- Using BNPL for food and essentials. We are concerned that using BNPL – which is a credit product – to pay for essential items is of itself a potential indicator of significant financial stress. In the absence of a broader understanding of affordable credit, this may feel like the only viable solution in some cases, but Consumer Association data shows this is a more expensive way to buy products than in mainstream supermarkets, so additionally comes with a premium for people who may already be struggling.

The future for BNPL

BNPL is growing in popularity at a time when many UK consumers are facing increasing pressures from the rising cost of living. Demand for credit is rising sharply and some people are faced with difficult choices about what they can buy and how they pay for it. MaPS, including through its MoneyHelper brand, wants to help people make informed choices looking across all the forms of credit available from high street lenders, BNPL providers and community finance products offered by Credit Unions and Community Development Finance Institutions.

In order to protect and improve people’s overall financial wellbeing, regulation of BNPL should address:

- Clarity. Ensuring that people using BNPL are aware of what they are committing to – a credit product – and the implications of missing payments. Consumer bodies and MaPS can help with this, and we will be updating the BNPL section of our MoneyHelper website to support enhanced public awareness of the potential risks

- Sharing data. BNPL providers and credit reference agencies continuing to work together to give a complete picture of a person’s creditworthiness and their ability to afford BNPL payments

We welcome the plans to tackle these issues, as published by the Government earlier this week

What’s next?

We will continue to monitor the use of BNPL using our Debt Need Survey as it evolves and use the insights that we gain to inform our policy positions.

Keep up to date with our debt advice work: register for our monthly newsletter and join the conversation on LinkedIn and Twitter.