Debt Insight Manager Paul Das shares what we know about the changes in how many people need debt advice, who might need advice in the future and how people are responding to changes in the cost of living.

In 2021, MaPS adopted a new way of measuring the need for debt advice and we reported back on who needed debt advice using the results from our 2021 debt need survey, including an explainer on the new measure.

The survey gives us insights on a broad cross section of society including ethnic minority, socially deprived and rural communities. The survey evolves to keep us informed about changes in society and in our 2022 survey we asked people what they were doing in response to changes to the cost of living.

How many people need debt advice?

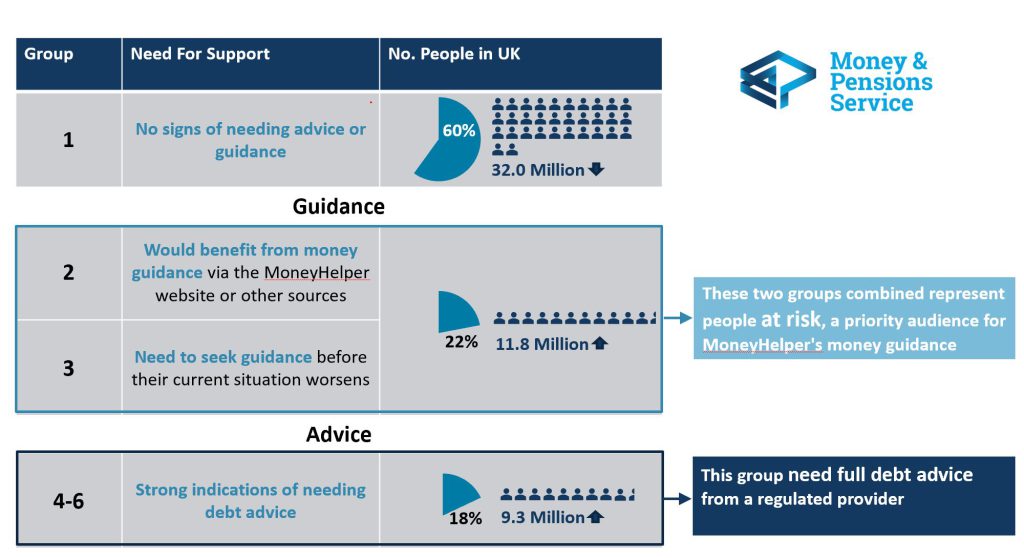

The size of each group in August-September 2022, when we ran the survey, is shown below along with a description of each group’s need for debt advice.

- Most people in the UK, 60%, were in group 1 and didn’t need debt advice (down 4% or around 2.0 million people compared to 2021).

- A further 22% were in groups 2 or 3 which we term ‘at risk’. An increase of just over 2% or 1.2 million people.

- Finally, 18% of the UK adult population needed debt advice, around 9.3 million people. This is an increase of 800,000 compared to 2021.

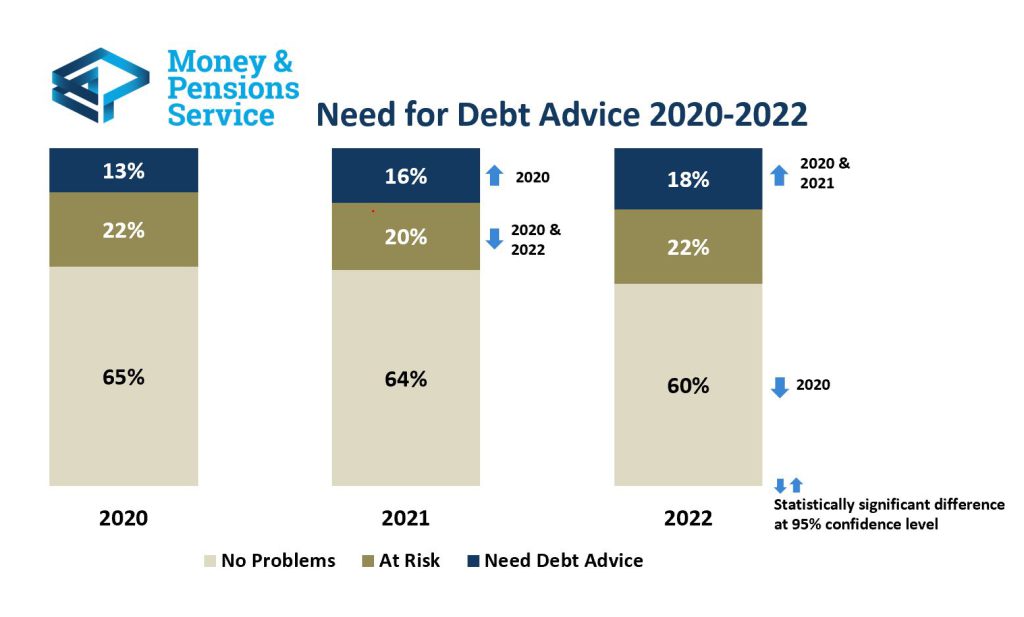

With this new survey, we are now in a position to look at how the need measure has changed over the past 3 years:

While the size of the at risk group has hovered between 20% and 22%, the proportion of people needing debt advice has increased significantly with a corresponding decline in the do not need advice group.

In the next section we take a look at the key changes to the people who need advice and those who are at risk.

Changes to the people who need debt advice

This group have not fundamentally changed in terms of their demographics. As we reported last year, they tend to be aged under 35, with children, on low incomes, renting their home and from minority communities. They also were more likely to have had an income shock in the previous three years.

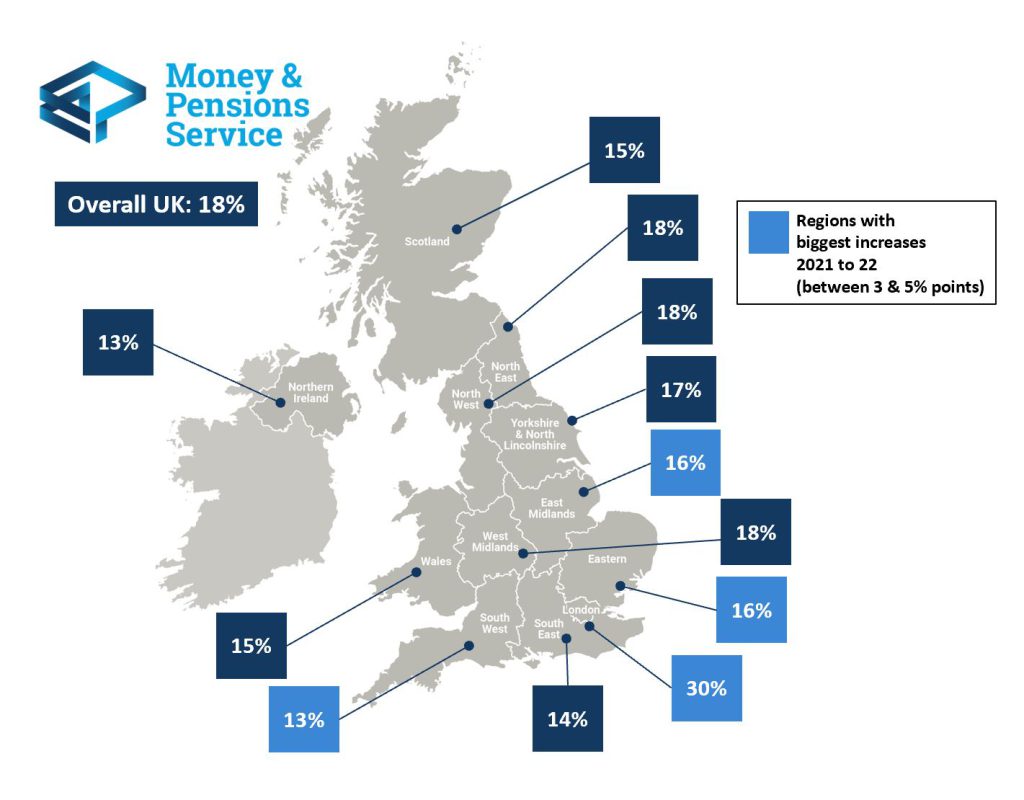

Looking back over time there have been some changes, however. The most notable change is how this group is now spread across the UK:

Devolved nation and regional need for debt advice

London continues to have the highest need for debt advice at 30%, up from 27% in 2021. The regions where indebtedness has historically been high remain the same – the North and West Midlands. But in 2022, the need for advice spread to the less densely populated English regions – the South West, East of England and East Midlands – regions that had been faring better until now.

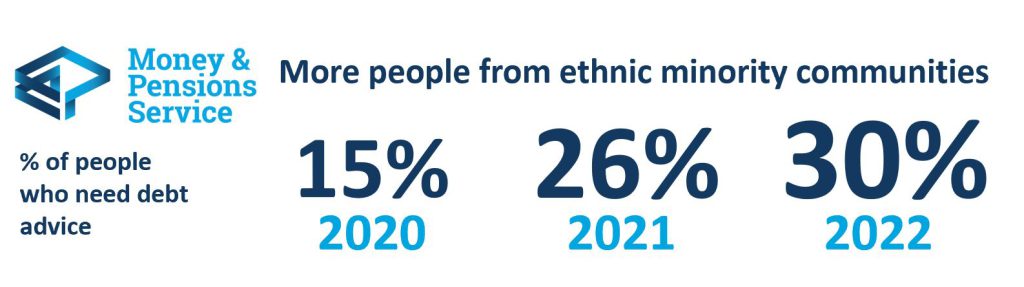

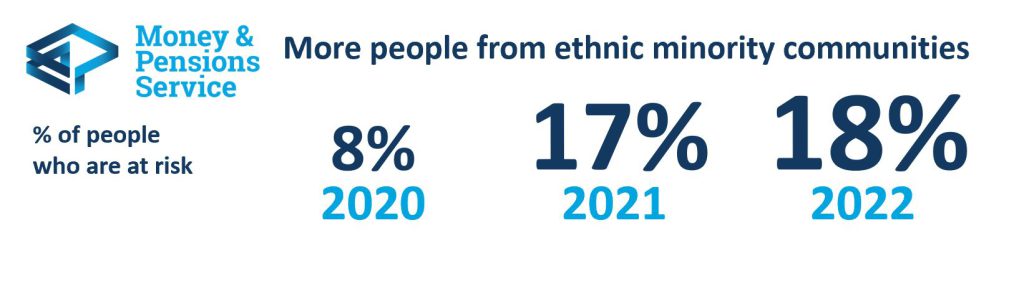

Another notable change to the people needing debt advice is a steep rise in the proportion of people from minority communities who need debt advice:

This is consistent with the findings of our evidence review of the Impact of Covid-19 on financial wellbeing which found that people from minority communities suffered more from labour market disruption as they are more likely to work in industries impacted by the pandemic.

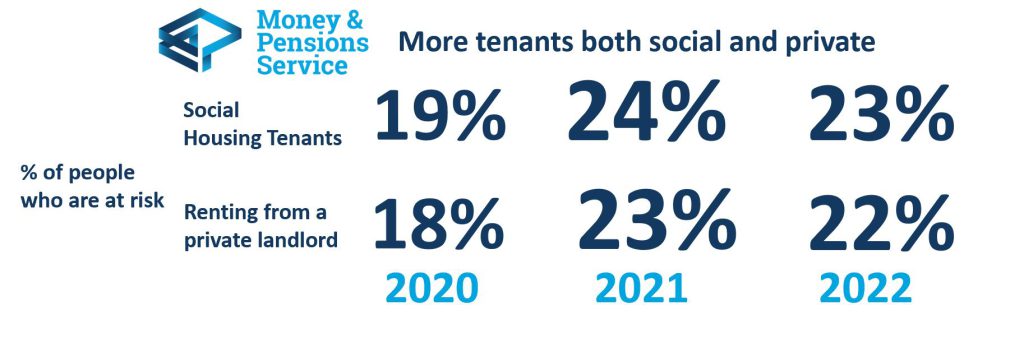

Finally, social housing tenants and home owners with a mortgage also make up a greater proportion of people needing advice. This is a cause of concern given the recent increases in mortgage rates:

Changes to the people who are at risk

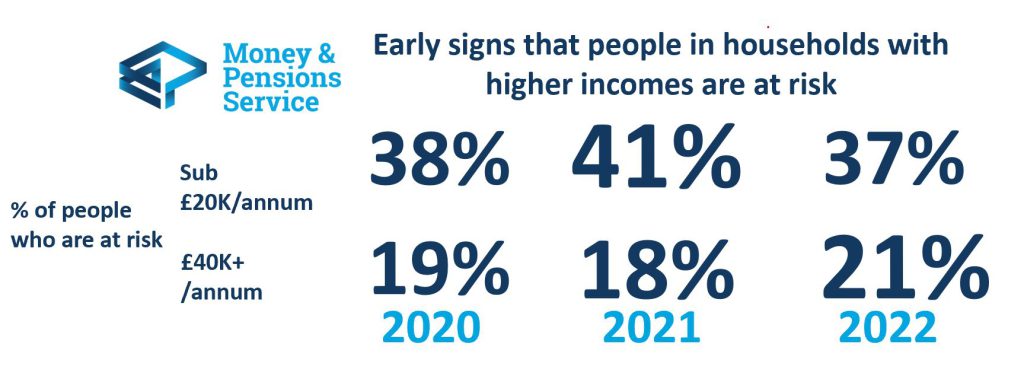

We see similar trends in the at risk group; people who don’t need full debt advice now but would benefit from money guidance and possibly more general advice to improve their situation. The proportion of people from minority communities in this group has doubled since 2020. It also contains more tenants and there has been a slight increase in households with an annual income of £40,000 +. This is could be an early indicator of higher income households being at risk.

Managing pressures on household finances

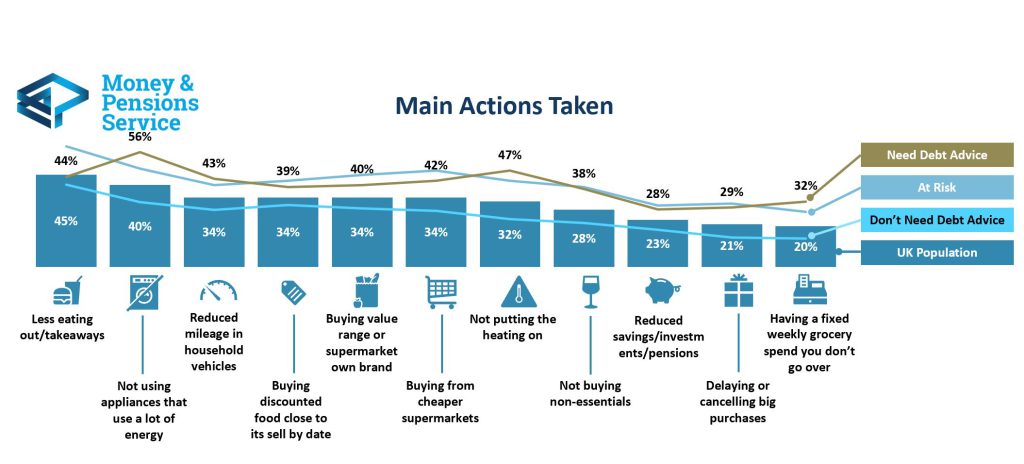

Over the past 12 months there has been a significant media focus on the action that households have been taking in response to changes in the cost of living. We reviewed a sample of these and in this year’s survey we decided to put some numbers behind each action by asking people what they had done in the last three months because of pressure on their household finances.

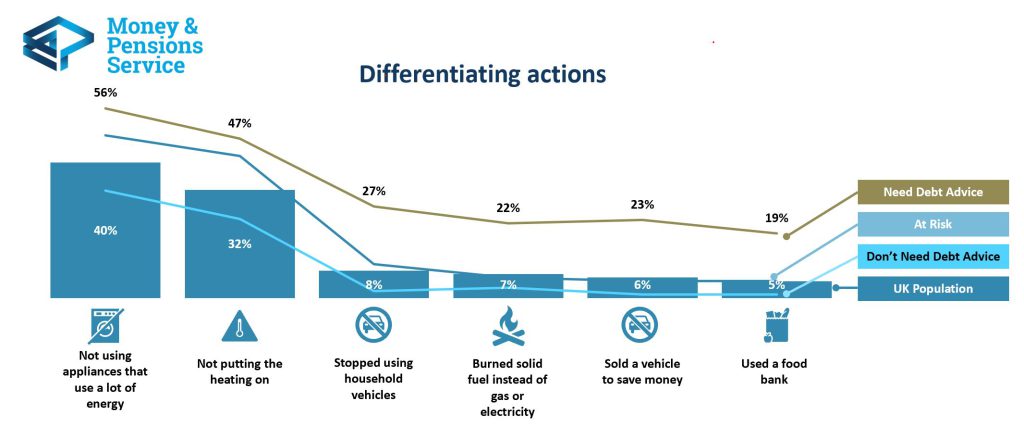

The first point to make is that most people are doing something, and this includes people who have no sign of having any debt problems. Eating out less and having fewer takeaways is something many people are doing. Only 20% said that they had not taken any of the 22 money saving measures that we asked about.

Driving less and saving money on food shopping are also actions that cut across different levels of indebtedness. However, a third (32%) of people who need debt advice are taking stronger action by having a firmly fixed grocery budget that they don’t go over.

There are other actions that make people who need debt advice stand out from the rest of UK population. More of them are cutting back on household energy, by reducing gas and electricity usage and, to a lesser extent, burning coal, wood or smokeless fuel instead. Around a quarter have cut back on using or sold vehicles and a fifth are using a food bank

Note: “UK population” percentages in the bars are based on the results from everyone interviewed in the Debt Need Survey. Detailed demographic quotas and weighting were used that accurately represent the UK population. The other percentages shown are based on the need debt advice group.

How the survey informs our policy decisions:

Learnings from the 2022 survey will allow us to:

- inform funding decisions for debt advice in the devolved nations

- profile people at risk of getting into problem debt and those who need debt advice now and how this is changing.

What’s next?

We will continue to use the new measure to monitor the need for debt advice in the UK and use the insights that we gain to inform our policy decisions and support the agencies we fund to deliver debt advice.

Keep up to date with our debt advice work: register for our monthly newsletter and join the conversation on LinkedIn and Twitter.