Earlier this year we published a blog on the overall findings of our latest Debt Need Survey, which measures the number of UK adults who need debt advice. Here, Debt Insight Manager Paul Das looks at what the survey tells us about the financial wellbeing of 18–24-year-olds in the UK.

Our definition of “needing debt advice” is that a person needs to go through a regulated advice process including a full review of a client’s personal circumstances, not just receiving general guidance. We define ‘strong indications of needing advice’ as being “currently behind on at least one priority bill, facing early or late-stage creditor action and using credit to pay for essentials”.

For the last three years, the survey has been telling us that younger people have a greater need for debt advice than those aged 25 and over.

This wasn’t a surprise because the results of our Adult Financial Wellbeing Survey 2021 show that 18–24-year-olds are especially likely to be “borrowing for the everyday”. By this, we mean using credit to pay for food and bills including borrowing from family and friends. People in this age group were also more likely to say that they found it a struggle to keep up with bills and credit commitments. The gap in borrowing for the everyday between this age group and older people has widened over time.

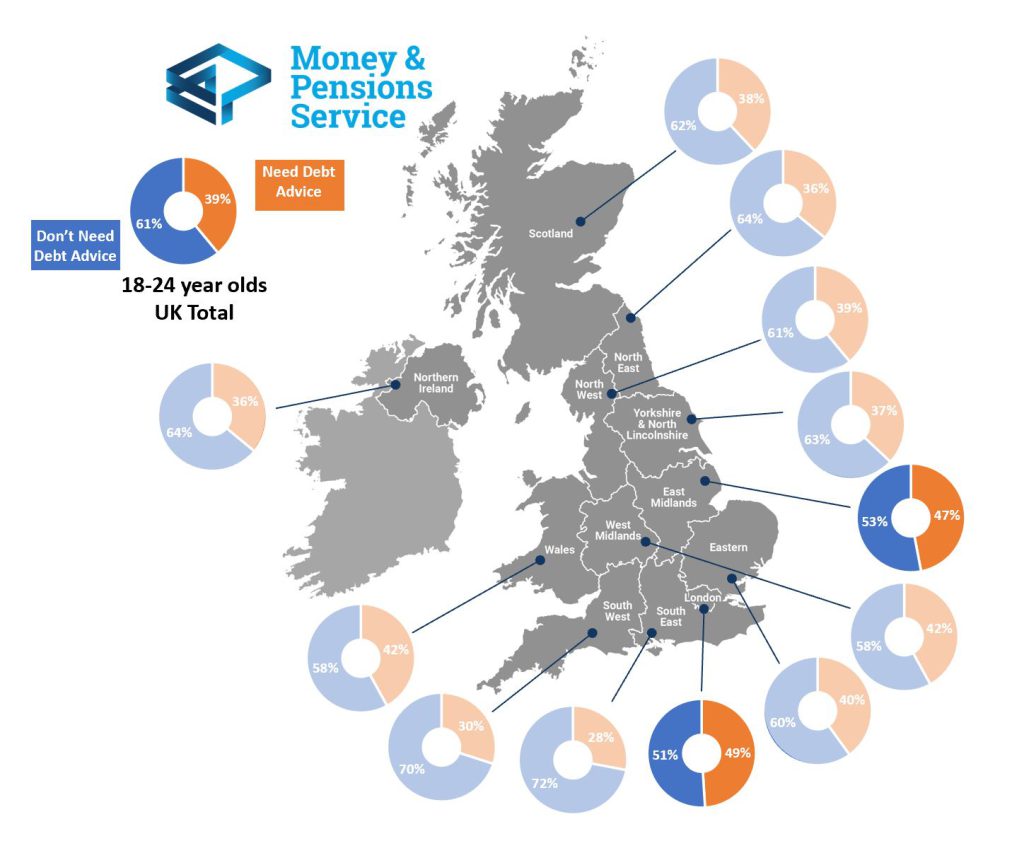

But what stood out in the findings of this year’s debt need survey is that nearly 4 in 10 (39%) of 18–24-year-olds need debt advice compared to 18% of the total population.

This raised two questions in my mind:

- Why have so many people got into financial difficulty early on in their financial lives?

- What about the other 61%? In what way are they different to those who need debt advice?

What’s different about these two groups?

I started off by looking at the profile of each group, 18–24-year-olds who need debt advice and people in the same age group who don’t. Despite the difference in their financial wellbeing, there are some similarities between them.

Personal income levels for the two groups are similar, at around £20,000 per annum, and so are their levels of education. Whether they needed advice or not, around half of the people in this age group were tenants (private or social). But more of those who didn’t need advice were living at home, possibly benefiting from a lower cost of living in their family home.

When you dig deeper into these young people’s circumstances, bigger differences emerge and you start to understand why some are more indebted than others. Those who need debt advice are spread across the UK, but the East Midlands and London were hotspots with close to half of this age group needing advice:

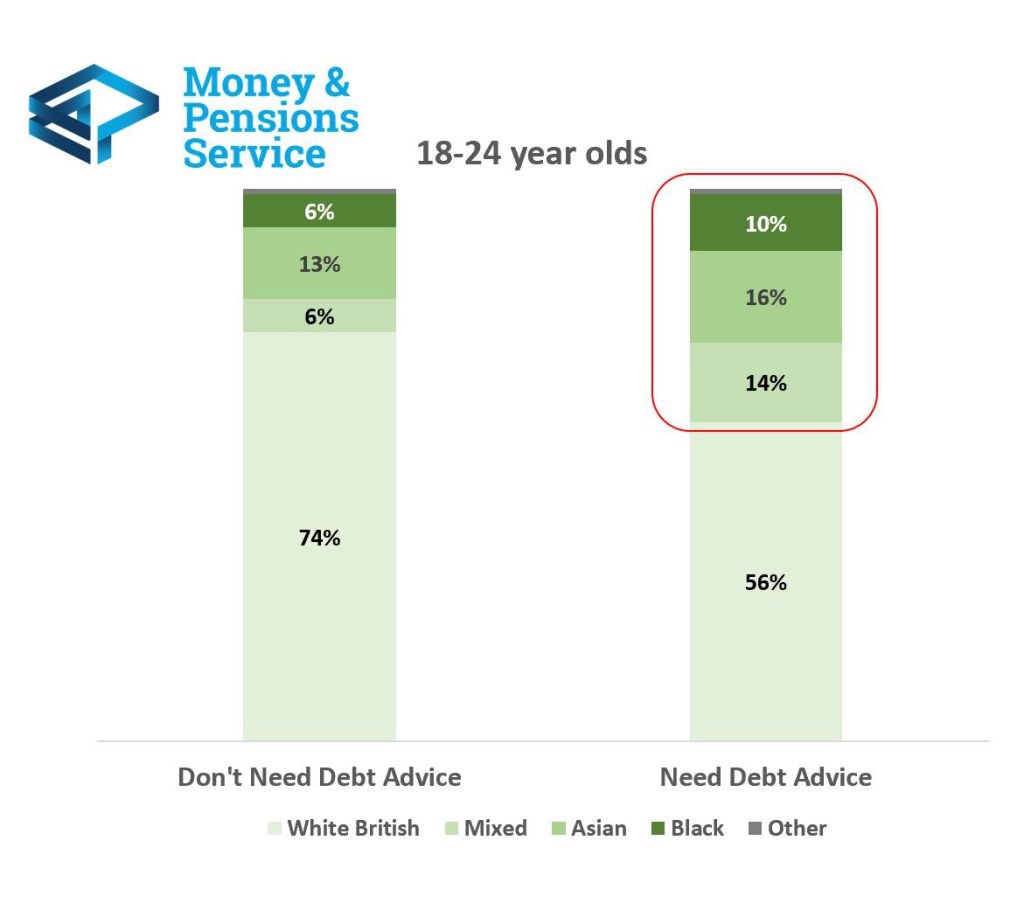

- Over a third of those needing debt advice (36%) live in the most deprived communities in the UK. People within this age group needing debt advice are also more likely to come from minority communities.

The impact of the type of work they do

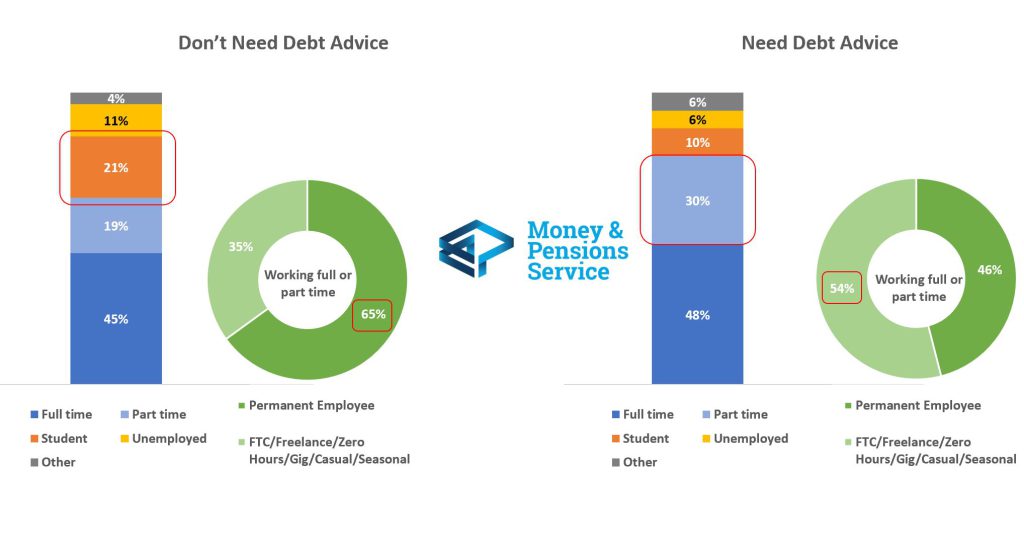

The biggest differences affecting whether these young people need debt advice or not relate to their working lives. More of the young people who need debt advice are working than those who don’t need advice (if you include part time employment). However, the terms and conditions that each group are employed on are different.

The young people who need debt advice have less secure employment, with just over half of those in work being on fixed term contracts, freelancers or other working arrangements with less reliable earnings such as zero hours contracts, the gig economy, casual or seasonal work.

Those who don’t need advice are more likely to be full time students and those who work are in permanent employment with more security and benefits. We should also bear in mind that people in this age group made up a large proportion of the workforce in the hospitality and retail sections in 2019 which were heavily impacted by pandemic lockdown restrictions.

Both groups face challenges in keeping up with bills and credit commitments and having a less stable income tips people over into needing debt advice.

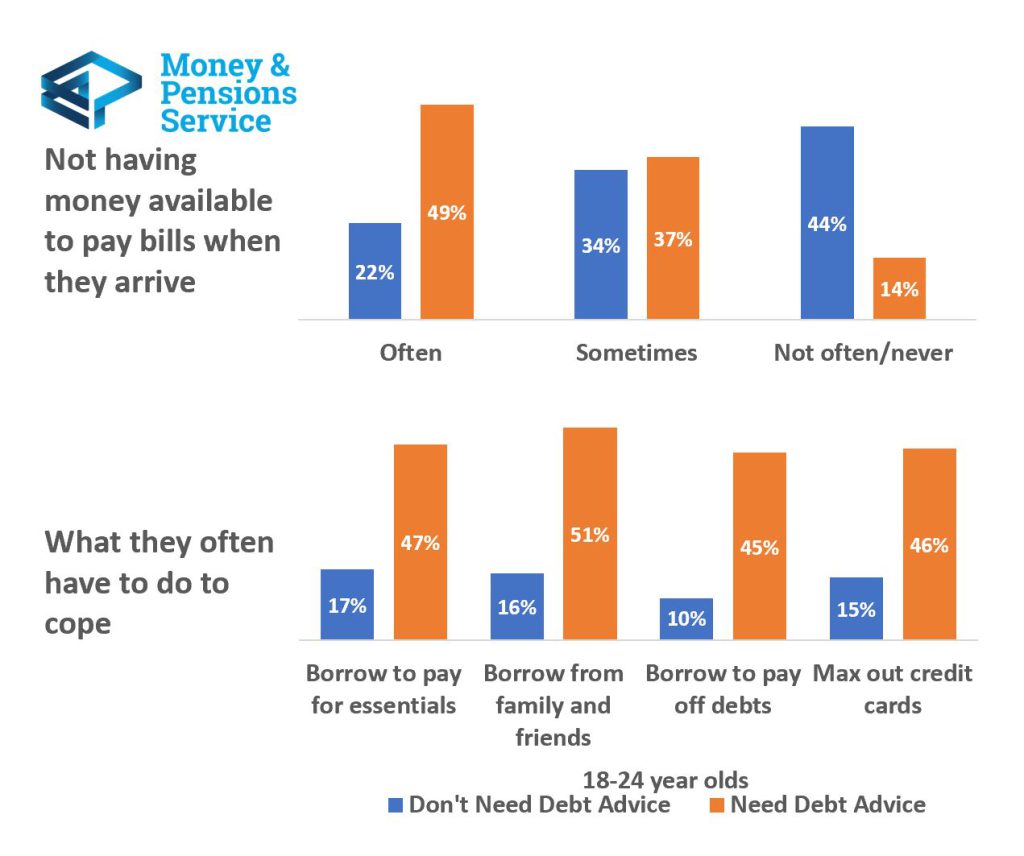

Around a third of both groups sometimes don’t have the money to pay their bills, but those who need advice experience this problem more often and around half are borrowing to get by. More of them are also using a flexible pay scheme to get access to their salary earlier than they are normally paid, but not all employers offer this of course.

Managing their money

Being in the early years of your working life, on a low income which might vary from month to month as the cost-of-living rises is a very challenging situation to be in. Faced with this, it is vital that young people in this position have the tools to help them manage their finances.

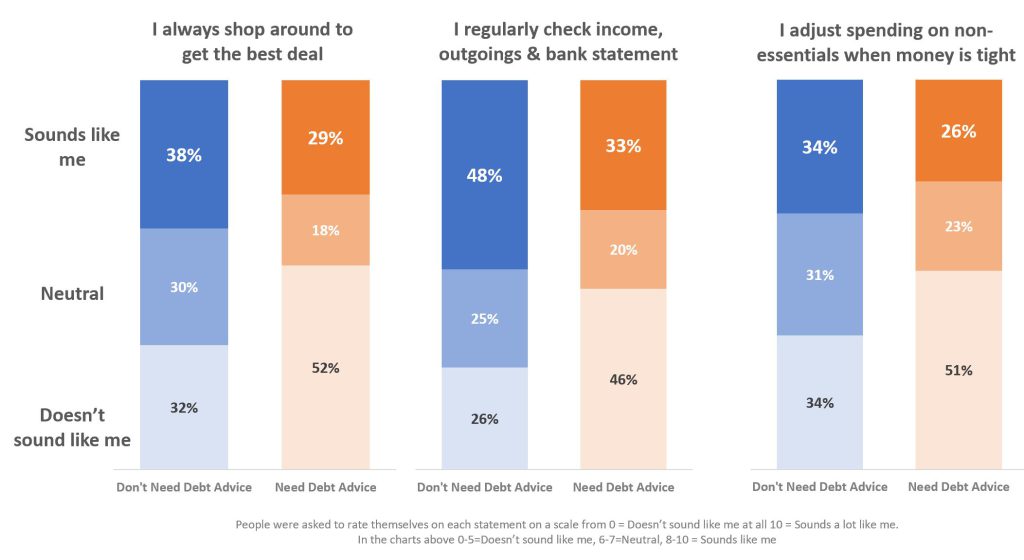

Managing money is difficult to do, and there are people in both groups who could do certain aspects of this better. However, overall young people who don’t need debt advice are better at managing and adjusting their spending, as well as being in a better position to start with.

However, we do also recognise that no amount of money management will overcome a deficit budget in which income is too small to cover essential living expenses.

How MaPS are helping

These findings emphasise the importance of one of the agendas for change from our UK Strategy for Financial Wellbeing – Financial Foundations. Our goal is for 2 million more children to receive meaningful financial education by 2030 so that they become adults able to make the most of their money and pensions.

There’s a lot of information and guidance on our MoneyHelper website including a guide for 16-24 year olds. There’s also help with the cost of living and a benefits calculator to check that people of all ages are receiving the support they are entitled to.

With this many young people struggling financially, investing in cryptocurrency can seem like a great side hustle to bring in more money. We have a guide on investing here covering risks as well as opportunities. We encourage young people or parents and carers to access these resources and wider services such as money guidance and debt advice

What’s next?

We will continue to monitor the need for debt advice in the UK and use the insights that we gain to inform our policy decisions and support the agencies we fund to deliver debt advice.

Keep up to date with our debt advice work: register for our monthly newsletter and join the conversation on LinkedIn and Twitter.